A FREE 2026 GUIDE FROM JANTZ WEALTH SOLUTIONS

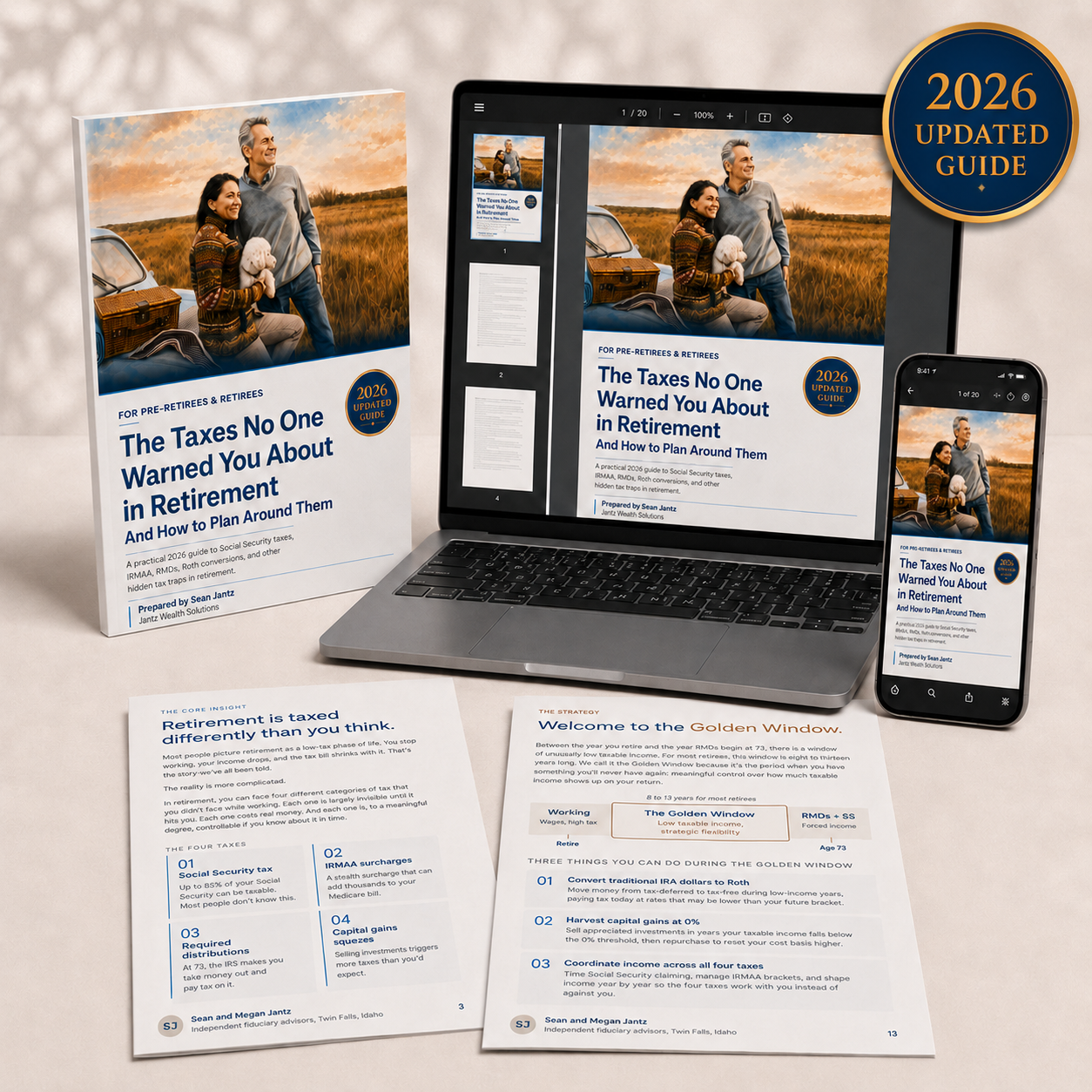

The taxes no one warned you about in retirement.

A practical 2026 guide to Social Security taxation, IRMAA surcharges, RMDs, the capital gains squeeze, and the planning window where coordinated decisions can avoid most of them.

- The four hidden tax cascades most retirees never see coming

- The eight-to-thirteen-year window where coordinated planning matters most

- Three concrete things you can do this week to find your own window

DOWNLOAD THE FREE GUIDE

Send me the 2026 retirement tax guide.

No spam. Unsubscribe anytime.